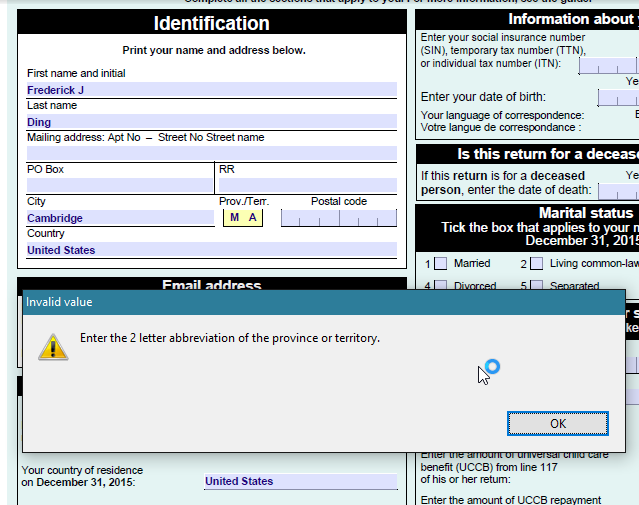

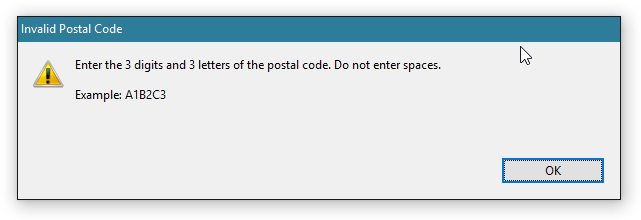

While trying to file my Canadian taxes as a nonresident, using the “Income Tax and Benefit Return for Non-residents … of Canada” — since I live in the United States and am a tax resident of the United States — I ran into a really frustrating bug in the first 5 form fields.

The form doesn’t accept non-Canadian provinces/territories and postal codes!

MA? not allowed.ZIP code? not allowed.

It’s really foolish, because many of the people who would be filing this form are likely residing outside of Canada. That’s why this version of the T1 return has an added Country field in the address block.

This is the kind of situation when PDF forms should just step back and allow free-form, unvalidated input.

TL;DR many Canadians in the US have more ways to vote, even under the 5-year limit, than previously thought.

A week ago, I mailed in my special ballot to Elections Canada. I can now say I’ve voted in the 2015 Canadian federal election!

There’s been a lot of discussion among Canadians at HLS, and folks in the Harvard Graduate Student Canadian Club, about the logistics of voting in this election. Notably, while most of them don’t have to deal with having a green card (as I do), some grad students may question how the 5-year limit applies to them.

Letters from Elections Canada, sent to two students who emailed them to inquire about logistics, support two conclusions.

1. Voting physically in Canada still possible

Voters who have been living abroad for 5 consecutive years or more and who are not exempt from the 5 year limit may vote in person at the advance polling station or the regular polling station corresponding to an address for which they have a proof of address (they cannot vote by special ballot).

– Elections Canada, in response to Peter W[1]

The provisions of the Canada Elections Act that prohibit registering to vote by mail from abroad after five years only apply to the special ballot. If you are a Canadian who has been a nonresident for more than five years, apparently you can still vote in person. (Canadian news has reported instances of people successfully using this “loophole.”) Advance voting days are October 9–12, conveniently during Canadian Thanksgiving and Columbus Day in the US.

2. Fluid definition of residency—unlike taxation and immigration

Thank you for your email … in which you requested information for students who have been living outside for more than five years. There is no differentiation between student voters abroad and non-student voters abroad; the five-year rule remains the same.

I would like to take this opportunity to clarify that there is no minimum period of time that an elector must have been in Canada in order to be considered as having resided there. It is based on where you consider your home address to be and the date of departure is based on the last day you consider yourself having lived in Canada.

– Elections Canada, in response to Peter W[2]

“Residing” has been interpreted here in the most liberal way possible by Elections Canada. It’s as though they are trying to preserve the broadest scope of voting rights possible in light of the Court of Appeal for Ontario ruling. (Good for them!)

The paragraphs quoted provide the basis for this interpretation:

Any instance of physical presence in Canada can be enough to renew your date of departure if you considered yourself to have lived in Canada during that stay.[3]

Elections Canada is not asserting an objective test of residency. They are not inquiring into whether the U.S. Department of Homeland Security treats you as a resident alien. They do not care when you became a nonresident for tax purposes on the CRA’s books.

So, in my interpretation, the following example set of facts satisfies their criteria and entitles the citizen to register to vote by special ballot (critical facts highlighted):

Alice is a Canadian citizen.

Alice is 23 years old.

Alice ordinarily lives in a rented apartment in Cambridge, MA.

Alice attends HLS on an F-1 student visa.

Alice started studying in the U.S. on an F-1 visa 6 years ago, since August 2009.

Alice intends to return to live and work in Canada after graduation.

Alice last lived in the Trinity-Spadina riding in Toronto, ON, before becoming a student in the U.S.

Alice last visited her parents on September 1, 2015, at that same residence in Toronto, for one day. She left on September 2.

Alice does not consider any other place to be her permanent place of abode.

Alice considered herself to have lived in Canada during that day. (remember, “no minimum period of time” is necessary)

Alice is a temporary resident outside Canada for fewer than five years, and may register to vote by special ballot with a departure date of September 2, 2015.

For an alternative hypothetical, see footnote 4.[4] Remember that these are only predictions of eligibility.

TL;DR many Canadians in the US have more ways to vote, even under the 5-year limit, than previously thought.

Again, just a reminder: I’m not a lawyer (yet). Don’t take this as legal advice. Do take it as the opinion of someone who believes the right to vote is constitutionally guaranteed to all Canadian citizens, and who wouldn’t mind seeing this tested in a legal challenge.

There is a textualist reading of the statute that supports this interpretation, based on the term “consecutive,” which would be interrupted by stays in Canada. See Canada Elections Act, S.C. 2000, c 9, § 222(1)(b) (applying the five-year limit to those “residing outside Canada for less than five consecutive years”).

Bob is a 22-year-old Canadian citizen, who works in New York City on post-completion OPT on an F-1 visa after graduating from a 4-year undergraduate in the U.S. Prior to his undergrad, Bob lived with his parents in Markham and considers this to be his home address in Canada. He has been in his F-1 status for 62 months, and is considered a US resident alien for tax purposes. Bob visited his girlfriend in downtown Toronto for a week during the summer, living at her apartment there. Bob intends to return to Canada upon the expiration of his F-1 visa. Bob may register to vote by special ballot in the Markham—Unionville riding, using the departure date following his stay during the summer.

After Elections Canada’s letter requesting my intended date of return, I responded by postal mail declaring a future date that should accommodate my intended career development in the United States. Needless to say, that intended date was pretty far into the future. At the close of my letter, I stressed that the Canada Elections Act has no statutory time limit on the intention to return:

I also write to emphasize that I became a nonresident of Canada upon acquiring residence in the United States on ****** **, 2014. Therefore, I am within the five-year limit on actual time abroad recently reinstated by the Court of Appeal for Ontario, even if my intended return would be beyond five years, since the applicable statute imposes no temporal restriction on the intended date of return for an eligible elector “who… (c) intends to return to Canada to resume residence in the future.” Canada Elections Act, S.C. 2000, c. 9, § 222(1).

I look forward to receiving a special ballot from your office at the upcoming election.

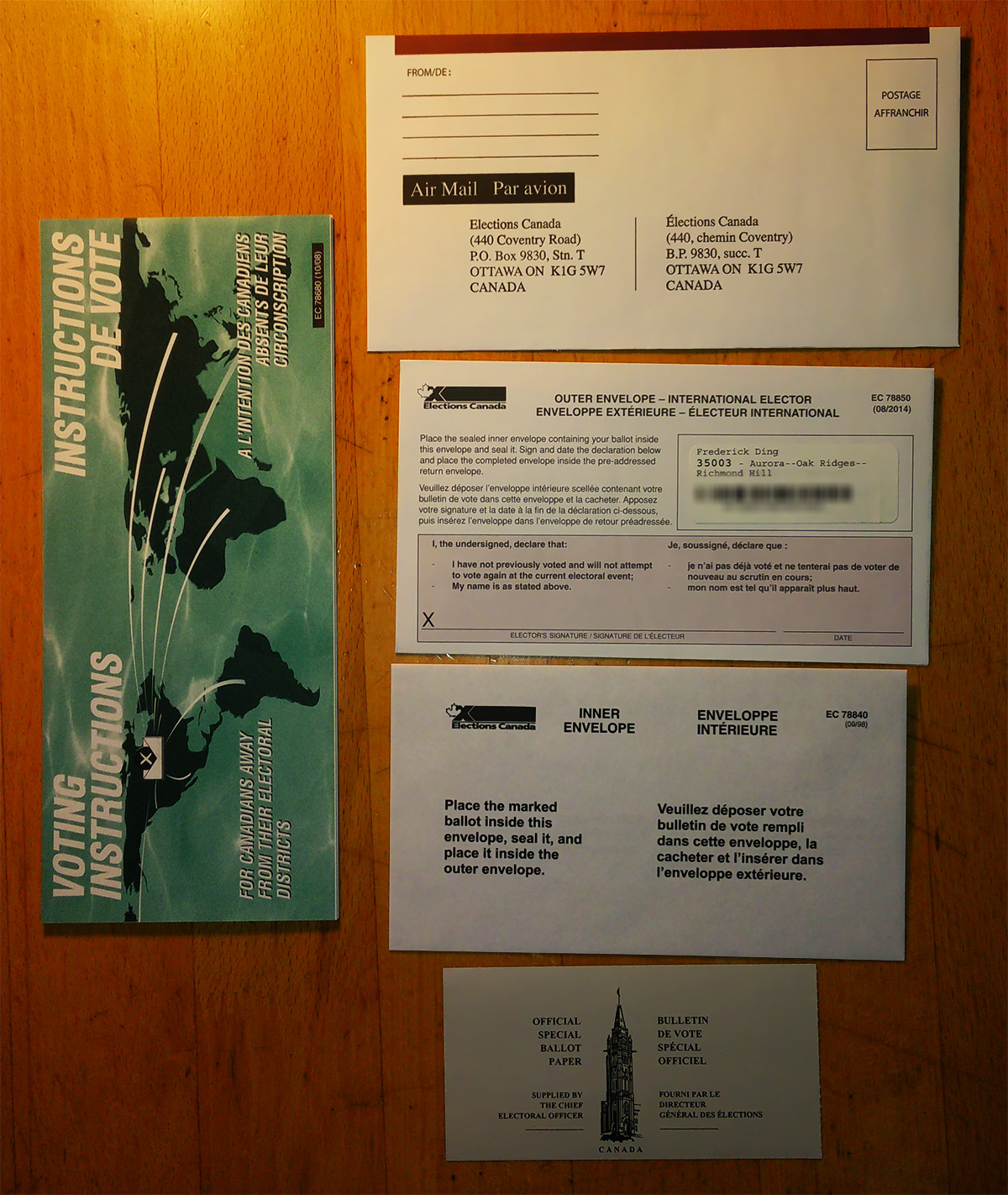

This week, I received the special ballot voting kit, which includes a guide pamphlet, ballot paper, an inner envelope, an outer envelope, and a preaddressed envelope.

Voting kit for special ballot

* As far as I am aware (and yes, I’ve checked), it is not illegal in Canada or Ontario to photograph this kit, provided that no vote has been marked. I haven’t yet decided for whom I will vote, so this photography serves simply as an illustration of what to expect for Canadian expats, rather than as evidence of my vote.

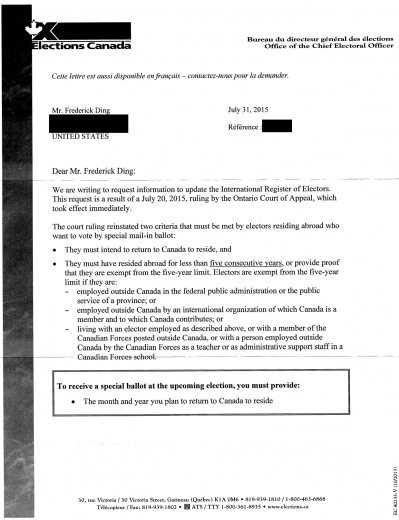

We are writing to request information to update the International Register of Electors. This request is a result of a July 20, 2015, ruling by the Ontario Court of Appeal, which took effect immediately.

… To receive a special ballot at the upcoming election, you must provide:

– The month and year you plan to return to Canada to reside

The implementation of this ruling demonstrates the imperfect nature of restrictions on expat voting—not only does the law have an arbitrary 5-year bar on voting from abroad, but for all expatriates Elections Canada is demanding a crystal clear declaration of the date they will return to Canada.

I think it’s worth noting that the underlying text of the statuteonly requires that an eligible elector “intends to return to Canada to resume residence in the future.” Canada Elections Act, S.C. 2000, c. 9, § 222(1)(c).

The agency could likely have fulfilled the statutory requirement by requiring only a simple checkbox that I do, in fact, intend to return to Canada “at some time in the future.” But that’s not what they did.

Wikipedia’s page on Elections in Canada lacked any mention of the expat situation, erroneously claiming (though it used to be true for 14 months) that “National voting is available to all Canadian citizens aged 18 or older.”

I rectified the second situation by revising those sentences and adding a section on expat voting to clarify the current state of affairs.

I believe my summary, which recalls the five-year limit’s origins in 1993, is the most compact summary of the whole picture, to date, in one place.

Of course, I humbly encourage others to contribute to Wikipedia and edit the article to continue improving its content, but I think the section I mentioned is worth quoting:

Although Section Three of the Canadian Charter of Rights and Freedoms provides that “every citizen of Canada has the right to vote”,[9] in practice only those citizens 18 years of age or older, and who reside in Canada or have been abroad for fewer than five years, may vote.[10] Exemptions to the five-year limit exist for members of the Canadian Armed Forces, employees of the federal or a provincial government who are abroad, employees of certain international organizations, and their cohabitants.[10] The five-year limit was originally enacted as part of Bill C-114, An Act to Amend the Canada Elections Act, in 1993; these amendments extended the special ballot to certain prisoners, and Canadians “living or travelling” abroad.[11] In September 2005, Jean-Pierre Kingsley, then the Chief Electoral Officer of Canada for 15 years, explicitly recommended in his official report that Parliament remove the five-year limit by amendment, but no action was taken.[12][13]

In May 2014, a court decision from the Ontario Superior Court of Justice invalidated the five-year limit as an unconstitutional restriction on the right to vote, in violation of Section Three, leading to a period of fourteen months during which all Canadian expatriates could apply to be on the register of electors.[14] However, the decision was reversed 2-1 on appeal at the Court of Appeal for Ontario on July 20, 2015, in a judicial opinion citing Canada’s history of using a residence-based electoral district system and a justification based on social contract theory, which held that the five-year limit was a permissible limitation of the constitutional right to vote under Section One.[15][16] As of August 2015, Elections Canada has implemented changes to its registration process to comply with the latest court ruling, and will require expatriates already on the register to declare an intended date of return.[17]

Again, I really hope this is appealed to the Supreme Court of Canada. Unfortunately, with the federal election just having been called for October 2015, it is impossible for any ruling to take effect in time for the impending election. (A legislative solution is also possible, but a court ruling would be the most optimal outcome.)

As a Canadian expat (US green card holder), I sincerely hope this case is overturned on appeal to the Supreme Court of Canada.

Like the respondents, who “attended university in the U.S. and remained there to pursue careers in their chosen professions”, my choice to be in the United States to advance my studies and career in the law is a matter of circumstance. Acquiring a green card did not signal the surrender of my citizenship and all its rights, responsibilities, and privileges.

It’s already annoying enough when the tax agencies of the two countries—CRA and IRS—use different definitions of residency for tax purposes… which differ from the governments’ definitions of residency for immigration purposes… which apparently differ from some U.S. states’ definitions of residency for driver’s licences…

… but now to convolute the meaning of a citizen’s right with a resident’s right?

I remain invested in the direction of the Canadian government and try to stay informed about Canadian politics. I still receive communications from multiple Canadian parties, am a supporter of two activist groups involved in IP and media law, and continue to engage in discourse with resident Canadians about the state of the nation.

As an individual with only one citizenship—Canadian—being disenfranchised at the end of five years from voting in Canadian federal elections would leave me with no democratic representation in any jurisdiction, since noncitizens in America are forbidden from participating in the U.S. electoral system even as a donor to any campaign. Even Canadian felons would have more political representation than I would have. This untenable situation would reasonably drive an expat to pursue foreign citizenship, if only to regain those rights and privileges that one would have expected Canadian citizenship to guarantee.[1]

The Charter doesn’t define the right to vote by residency, but by citizenship. Section 3 provides:

Every citizen of Canada has the right to vote in an election of the members of the House of Commons or of a legislative assembly and to be qualified for membership therein.

The majority opinion contends that residency has been historically a factor in implementing the electoral system that enables citizens to exercise the right to vote, but the court erroneously conflates the implementation of a constitutional right with the acceptable boundaries on that right.

It embraces the vague notion of protecting the “social contract”, a principle in which individuals who make laws must also obey them, as a legitimate purpose to restrict the voting rights of expatriates. But really, expatriates remain bound by Canadian laws, particularly those affecting taxation, citizenship, and property…[2] Laws passed in Canada, far from having “little to no practical consequences” for my expat family as the majority opinion contends, affect us financially (at least in terms of loans and taxes), affect my parents’ property and retirement assets and income, and influence our choices later down the road about whether or not to return to Canada.

… and it’s not like every resident citizen is affected by every law anyways! Bear with me for a moment; consider this perspective: the scope of a law often excludes those people who supported it. A law limiting concealed carry handguns, for instance, would probably be passed by those people who themselves have no need or desire to engage in the actions that the law prohibits. Indeed, this ruling actually enables resident citizens to violate the social contract principle supposedly being protected: a hypothetical law imposing 50% taxes on foreign income earned by nonresident citizens, for example, could be passed by representatives of resident citizens living comfortably in Vancouver and Toronto unaffected, while disenfranchised citizens abroad would be the ones affected.

This case better make its way to the Supreme Court of Canada.

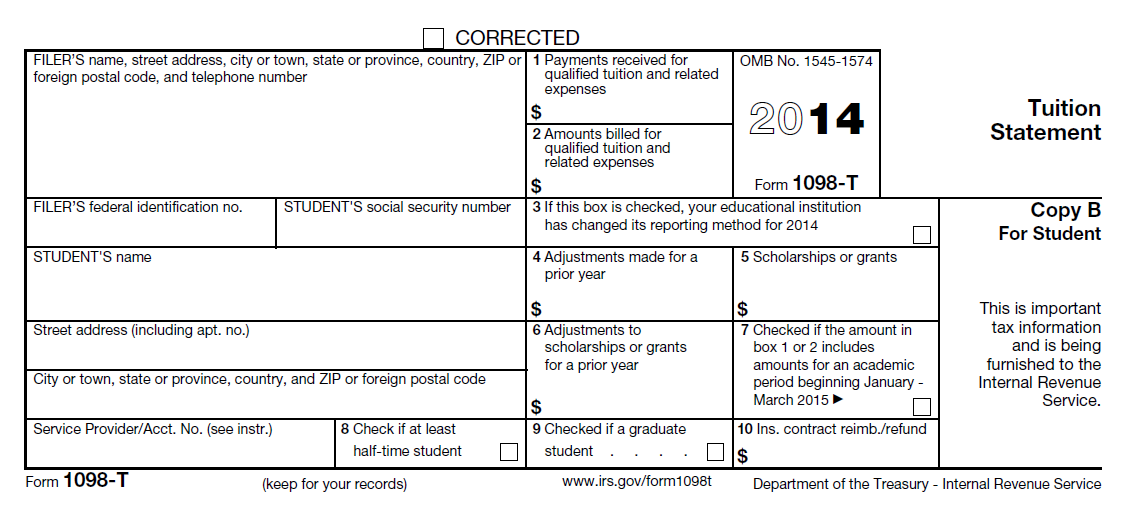

I am not a tax attorney or tax consultant. This post was written while I was an undergraduate student at the University of Pennsylvania, and Co-Chair of the International Student Advisory Board.

Universities often will choose not to issue this tuition statement to international students because those students can’t do anything with it. This is, however, an incorrect generalization.

Are international students able to use this form for anything?

Most international students are ineligible to claim those educational credits/deductions because they are nonresident aliens (e.g. F-1 student). These individuals would not benefit from having the 1098-T.

But some students, especially graduate students, may be eligible to claim credits/deductions because…

they are resident aliens under the substantial presence test, usually because they have stayed in the United States for more than 5 years;

they are nonresident aliens for immigration purposes, but resident aliens for tax purposes, maybe as spouses of American citizens or resident aliens; or

they are nonresident aliens for both immigration and tax purposes, but eligible dependents of parents who are resident aliens/permanent residents/citizens; those parents are able to claim these credits in certain situations.

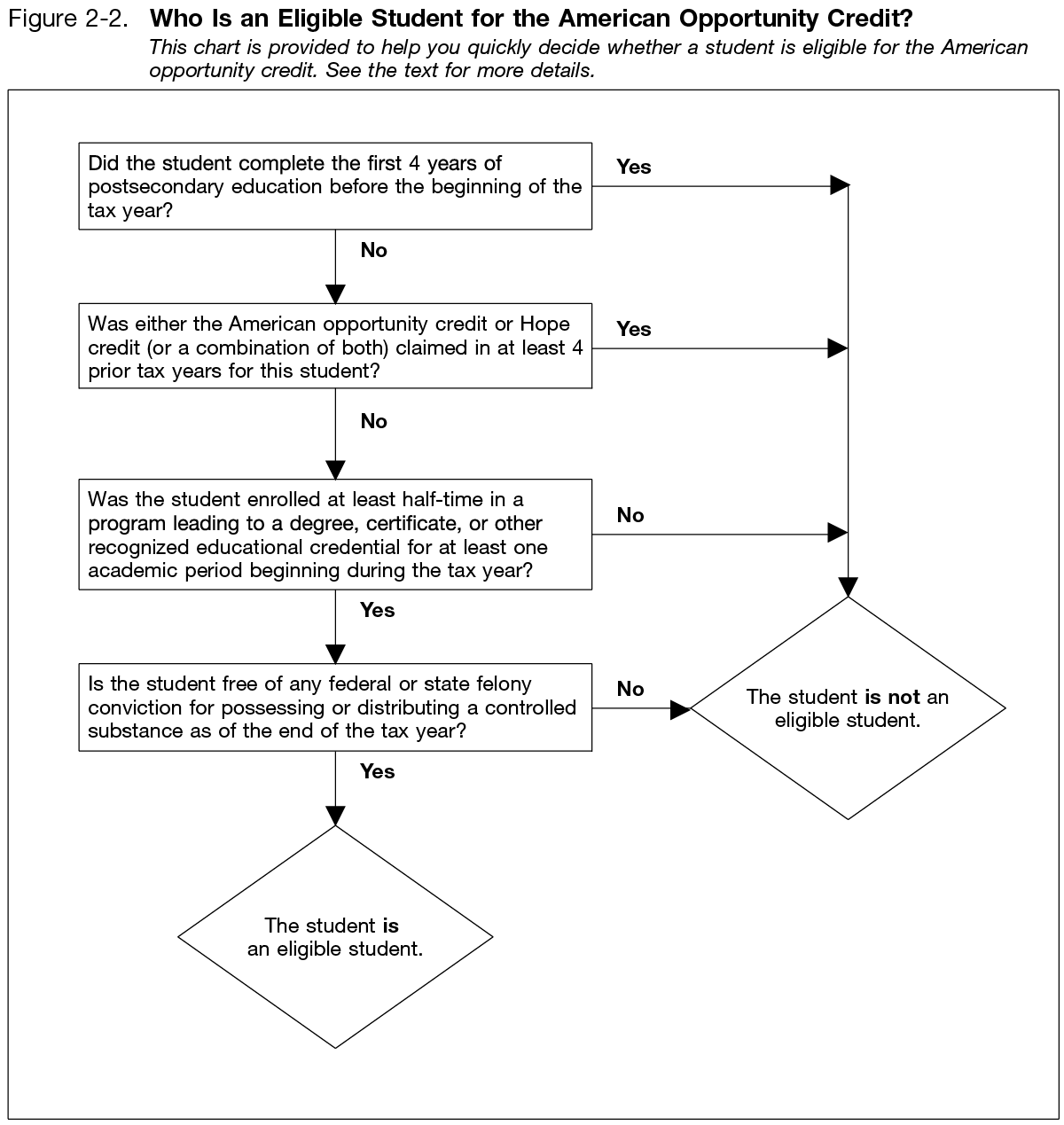

Figure 2-2 from IRS Publication 970, illustrating who is an eligible student for the American Opportunity Credit. Note: not all eligible students can claim. See Publication 970 for a flowchart of who is eligible to claim.

I am an international student in the above categories. Can I get a 1098-T from my school?

The IRS says that universities “do not have to file Form 1098-T or furnish a statement for… nonresident alien students, unless requested by the student“. Additionally, they are not required to provide it for “students whose qualified tuition and related expenses are entirely waived or paid entirely with scholarships”.

You must still meet all of the other requirements to get a 1098-T:

Attend an eligible educational institution (college, university, vocational school, or other postsecondary educational institution in §481 of the Higher Education Act)

Have paid qualified tuition and related expenses in that tax year

i.e. tuition, fees, course materials required to be enrolled

does not include room, board, insurance, medical expenses including student health fees, transportation, and personal/living/family expenses

Receive credit for the completion of course work leading to a postsecondary degree, certificate, or other recognized postsecondary educational credential

i.e. most undergraduate bachelors programs and graduate masters and PhDs qualify

Have provided your SSN or ITIN to the educational institution either through student records or an additional Form W-9S

What are some potential hurdles?

I was in a situation this year where my university did not issue me a 1098-T, and responded to my request with a form letter:

Does every Penn student receive a 1098-T? Penn does not provide a 1098-T to non-resident aliens, or any student whose qualified charges are fully funded by grant, scholarship or tuition waivers, or any student who was enrolled in non-credit courses during the academic year.

They additionally stated,

“Though you might have received a 1098t form in the past, going forward as a Canadian citizen you will not receive one.”

As I’ve explained above in this post, this determination was a mistake. It conflates citizenship & immigration status with residency for tax purposes, and ignores the possibility that someone else other than me may be eligible to claim the credit.

Furthermore, even if I were a nonresident alien ineligible to claim the credit, nothing in the IRS regulations for Form 1098-T gives the educational institution the right, responsibility, or power to determine whether I might be eligible to claim the credit; nor does it permit them to deny a Form 1098-T to a nonresident alien’s request.

What does this situation reveal about international students?

First, on the superficial level, this situation reveals that immigration status and residency for immigration purposes differs from tax status and residency for tax purposes. Clearly, not all employees who handle these cases are aware of these stipulations.

More importantly…

International students are a large, diverse, and varied community. International students have complex needs based on their individual families’ statuses. It is a mistake to define broad, indiscriminate policies that treat all international students identically.

If you think I’ve made a mistake in this post, or wish to disagree with my conclusion here, I’d like to hear from you. Comment below or send me an email using the contact form.

I respect the majority of this article. I agree with most of it — the North American medical education system is clunky, and a ton of hurdles are thrown in the way of students who want to become doctors.